Life Insurance Policy Business Definition

Compare Life Insurance

Take care of what matters most - we outline how to get the right life insurance policy to protect your family

Updated 19 October 2021

What is life insurance?

Life insurance is a type of insurance contract which pays your dependants a fixed lump sum if you die during the term of the contract. The cost of a life insurance policy depends on many factors including how much cover you want, your age, gender, whether you smoke and overall health and lifestyle.

Summary of Life Insurance

- The cost of Life Insurance is very competitive in New Zealand and the existence of price comparison websites to show quotes makes it more affordable than ever before.

- Getting the right cover level is the most significant consideration - popular practice is to insure for 10X your pre-tax salary. For example, if you earn $75,000 per year, it is reasonable to insure for $750,000. However, this is not always the best approach - our life insurance calculator offers a more extensive assessment.

- When it comes to buying life insurance, shop around. In some instances, we found price comparison sites quoted the same policies offered by the insurers directly for HALF the price.

- A 30-year-old male/female non-smoker should be able to get a $500,000 policy for under $400/year by shopping around. As to be expected, policies get more expensive the older you are.

- Insurance brokers offer expertise and know the market more than anyone - if you have a specific concern, health issue or question about anything related to life insurance, they will likely be your best resource and asset for picking the best policy.

Know this: Before making any policy

switch, it's essential to

confirm that any exclusions you have on your previous policy will be covered on your new policy. This can catch people out who think they're covered but find themselves uninsured by exclusions. We are aware of New Zealanders switching policies without paying careful attention to any exclusions they may have. This has led to declined claims.

Our Life insurance guide covers:

Life Insurance – Why It's Important

It's a sad reality that one child in every 32 will lose a parent or guardian while under 18 in New Zealand. Grief and despair are often followed by the loss of an income and financial hardship for the family. Life insurance is an affordable way to help your family and avoid financial suffering if the worst happens.

What's important is making sure you get the right policy and not to overpay. New Zealand has many sad examples of families overpaying $10,000+ over the life of policies which often don't offer the best benefits. We've put this guide together to explain life insurance, assess whether it's right for you and help you get the cheapest and best policies.

Life Insurance – the basics

- New Zealand insurers offer many different types of 'life insurance'.

- Some life insurance will only cover a mortgage, while other life insurance looks after all of your dependants.

- Our focus is on life insurance policies that cover your family if you (or your partner) were to die.

- Death is certain, but life insurance covers the possibility that you "may" die within a certain period of time.

- We believe that the reliance of a family on one parent's income is now so great any person with one or more dependants should at least consider taking out life insurance.

- In our review, we show premiums starting from $600 a year for two adults, offering a $500,000 payout. Insurers accept fortnightly policy payments to make managing bills easier.

Life Insurance in a Nutshell - Our View:

- Life insurance policy costs vary between insurers - comparing is the best way to get the best deal. Never go direct to an insurer without other quotes in hand.

- While Cigna appeared to be the best value life insurer from our quote sample, every person or couple will have different needs and expectations.

- We strongly suggest using a comparison tool;LifeDirect is the most extensive and offers quotes from multiple leading life insurers such as Cigna, AIA, Fidelity and others. All have strong credit ratings, meaning the insurers will pay if you or your family need to claim. And, should you need to claim, LifeDirecthandles that too by liaising with the insurer.

8 Must-Know Life Insurance Facts

| |

Life insurance pays out a set dollar amount to your family if you die while the policy is valid

|

| |

Don't have dependants? You probably don't need life insurance

|

| |

What should my cover amount be? How long should I have the policy for?

In estimating your cover amount, add up:

OurLife Insurance Calculatorconsiders the above factors, among others, to predict a suitable number that would be sufficient for insurance. |

| |

Ask yourself - Should I get a joint policy with my partner, or two single policies?You can do either. In most cases, it's almost always cheaper than two single policies, and easier and quicker to set up than two single policies. If you split from your partner, your insurance premium can be re-assessed on an individual basis. |

| |

The lower the risk of your death, the cheaper your life insuranceLife insurance premiums increase with the likelihood of your death. A 30-year-old office worker will have a cheaper premium than a 90-year-old mountain climber. Specific factors include:

|

| |

Ongoing full disclosure is essentialThe cost of life insurance rises as you age above 35 years of age, and if you have had a health issue, your policy price will be affected. If you've had a health scare and failed to disclose that, there will be consequences later on as insurers are quick to refuse to pay based on "non-disclosure". Remember, a change in health means a change in premium, whereas non-disclosure means a policy will be invalid if claimed on. |

| |

Have a healthy lifestyle? You'll almost certainly get cheaper policiesFirstly, not smoking is going to save you thousands on life insurance. If you have just quit, you may also be covered – some policies require you to be smoke-free for at least 12 months, so it's worth checking. Again, it's all about disclosure. If you lie and continue to smoke, your policy could be invalid if you die. |

| |

Switching your policy may save you moneyIf you already have a life insurance policy, the best buy guide (below) may help you save what you pay each year if you decide to change policies. If a new quote for the same amount of covershows a cheaper price, all other things being the same, it's best to switch. Remember, buy the new cover and then, once it's valid, cancel your existing policy. Never go "between policies", i.e. cancel one while you shop around for another, as your beneficiaries won't receive any payout should you die in that time. We recommend you take your time in deciding, making sure the cover lines up with what your previous cover offered. Remember full disclosure is needed about any health issues, so don't try to save money by avoiding your obligation to declare recent problems. |

Life Insurance in a Nutshell - Our View:

- Life insurance policy costs vary between insurers - comparing is the best way to get the best deal. Never go direct to an insurer without other quotes in hand.

- While Cigna appeared to be the best value life insurer from our quote sample, every person or couple will have different needs and expectations.

- We strongly suggest using a comparison tool;LifeDirect is the most extensive and offers quotes from multiple leading life insurers such as Cigna, AIA, Fidelity and others. All have strong credit ratings, meaning the insurers will pay if you or your family need to claim. And, should you need to claim, LifeDirecthandles that too by liaising with the insurer.

Life Insurance Policy Comparison

How to save thousands on life insurance over your lifetime

- Firstly, never go directly to an insurer first. You'll pay full price and have nothing to compare with so it may (and probably won't) be the best deal.

- Instead, start with a comparison website like LifeDirect. They compare the latest prices from a select number of insurers and aim to give the consumer all of the relevant information to make a decision.LifeDirect does not give insurance advice.

- If you have a specialist health need, family situation and/or prefer to talk to someone directly, contacting an insurance broker is a sensible step.

Our Quotes

- We obtained multiple quotes from 10 insurers for three individual policies each requiring $500,000 of cover, as outlined below.

- While every policy is different, ourBest Buysdo indicate the range in price among insurers.

- The results are below, and indicate a large variation in pricing.

- Quotes for AIA, Asteron, Cigna, Fidelity, PartnersLifewere suppliedby LifeDirect and found to be the same (or cheaper) than going direct to the respective insurer.

| 30 YEAR OLD MALE | 35 YEAR OLD FEMALE and | 55 YEAR OLD MALE

|

Our quote data:

- Quotes presented above are BEFORE any Healthy Lifestyle discount, Member Discounts, first-year discounts and multiple insurance policy discounts etc and have been adjusted where necessary.

- Quotes exclude cashback offers, which are routinely available from select insurers.

- Annual pricing, paid upfront, generally offers the lowest cost policy. Paying fortnightly or monthly may lead to a higher overall annual cost for the same policy.

- Some insurers had some quote limitations, and we have made the following manual adjustments:

- Pinnacle Life - We have removed the first-year and variable discounts offered by Pinnacle Life to keep prices consistent with the way other insurers present their prices

- Cigna - offered monthly prices only, including 10% or 20% discount - our data grosses up the pricing to compare policies at their standard prices

- BNZ - offered monthly prices only - our data multiples the monthly price by 12. No joint policies available so separate quotes priced and combined.

- Fidelity - No joint policies available so separate quotes priced and combined.

- Southern Cross - offered monthly prices only - our data multiples the monthly price by 12. No joint policies available so separate quotes priced and combined.

- PartnersLife - No joint policies available so separate quotes priced and combined.

Life Insurance in a Nutshell - Our View:

- Life insurance policy costs vary between insurers - comparing is the best way to get the best deal. Never go direct to an insurer without other quotes in hand.

- While Cigna appeared to be the best value life insurer from our quote sample, every person or couple will have different needs and expectations.

- We strongly suggest using a comparison tool;LifeDirect is the most extensive and offers quotes from multiple leading life insurers such as Cigna, AIA, Fidelity and others. All have strong credit ratings, meaning the insurers will pay if you or your family need to claim. And, should you need to claim, LifeDirect handles that too by liaising with the insurer.

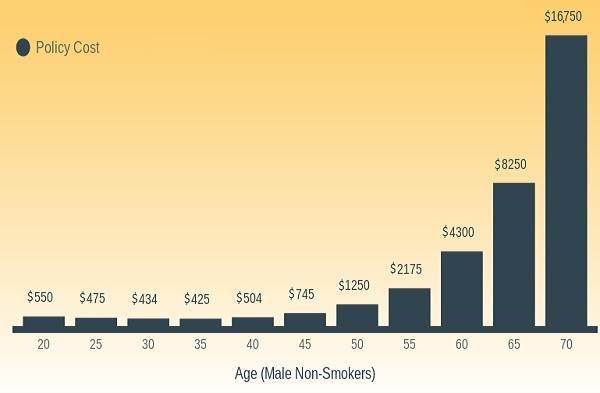

Figure 1 - Average Life Insurance Policy Cost by Age 20 - 70 (Male, Non-Smokers, $500,000 cover)

Top Tip - Getting Quotes WILL save you thousands over your lifetime

- Buying life insurance is not as transparent as it should be. Despite the number of providers in the market, there is an enormous range in cover.

- We found that specialist life insurers could offer better value than their competition, and that price comparison websites such as LifeDirect offered quotes from well-known brands which were, on occasions, cheaper than going directly to the insurer.

- In the last 12 months, many insurers have stopped selling life insurance, including AMI, State and OnePath. Long-time giant Sovereign became AIA. As a result of the consolidation, specialist life insurance companies are increasing their market share.

Life Insurance - Frequently Asked Questions

Life insurance can be complicated - our list of common queries helps you understand what's important. Do you have pre-existing health conditions? Our guide to life insurance cover with pre-existing conditions has you covered.

I've heard about "Family Protection Insurance" – what is the difference between that and life insurance, and which is better?

- Family Protection Insurance is a specialist insurance policy that provides a monthly payment to your family for a fixed number of years after you die. You pick the amount, and following death or diagnosis of terminal illness, your family gets the amount tax-free every month.

- Family Protection Insurancesuits young families who will need money as the children grow up, receiving a monthly lump sum rather than a once-only payout.

- Family Protection Insurance can work out cheaper than life insurance, but it depends on how much you insure for and your age.

- Insurers suggest that Family Protection Insurance "compliments" life insurance, providing regular income while life insurance is used to clear debts. We disagree – one or the other will most often be sufficient for looking after your family in the long term if you insure for the right amount.

To give the best comparison, we've taken three examples:

1. Nathan and Aroha (both 35, with two children) want to insure for $1.2m

- Using life insurance (lump sum payout), the cheapest premium we found was $1,274.58 per year.

- Using Family Protection Insurance, $10,000 per month (totalling $1.2m after 10 years) the cheapest premium we found was $1,149.72 per year, 10% cheaper than the life insurance quote.

2. Mike and Jenna are both 50 and want to insure for $1.2m

- Using life insurance, the cheapest premium we found was $4,126 per year.

- Using Family Protection Insurance, $10,000 per month (totalling $1.2m after 10 years) the cheapest premium we found was $3,747.48, 10% cheaper than the life insurance quote.

3. Roslyn and Jeremy are both 40 and want to insure for $600,000

- Using life insurance, the cheapest premium we found was $883.79 per year.

- Using Family Protection Insurance, $5,000 per month (totalling $500,000 after 10 years) the cheapest premium we found was $829.32, 6% cheaper than the life insurance quote.

Why do you suggest insuring for "10 times the salary of the highest earner"?

When a parent dies, there needs to be enough money to cover a mortgage and ongoing expenses. Insuring for 10 times the salary of the highest earner allows an excellent cushion to keep the family in good financial health even if the surviving parent stays at home to look after the children. Just insuring to pay a mortgage doesn't help with any other family expenses, causing great stress in the long term.

When should I get a life insurance policy?

Usually the most popular time is as soon as someone relies on your income, such as a partner and/or child. It's not a comfortable feeling to insure your life, but the benefits are tremendous to your family should the unthinkable happen. If you are young, life insurance will cost less as younger people are (on the whole) healthier than older people, who pay substantially more as the risk they will die is higher. Please see our table below which illustrates this point.

The annual cost of life insurance for a $500,000 payout taken out at different ages (non-smoker, male):

- 25 years old: $475.40

- 35 years old: $446.00

- 45 years old: $705.40

- 55 years old: $1,999.40

I've been offered "critical illness cover" with my life insurance policy. Should I get this?

It depends. We see many problems with critical illness cover. Firstly, it only covers specific illnesses, so while "cancer" is covered, melanoma, prostate and skin cancer probably are not. And "strokes" have their own exclusions. We're not big fans of critical illness insurance. If you think you should get it for a specific reason, we suggest speaking to an insurance broker to ensure you make the best decision.

Concluding Comments: Buying a Life Insurance Policy - Balancing Price and Coverage

There is a lot of money to be made from selling life insurance, and for this reason banks and other companies offer it as an add-on service. When it comes to getting the best insurance, it's a balance ofpriceandcoverage. Don't be tempted by a cheap policy with a lot of exclusions - life is unpredictable and you want a policy that is clear. If in doubt about anything, talk to an insurance broker - they work with you to find the best policy to suit your situation.

Life Insurance in a Nutshell - Our View:

- Life insurance policy costs vary between insurers - comparing is the best way to get the best deal. Never go direct to an insurer without other quotes in hand.

- While Cigna appeared to be the best value life insurer from our quote sample, every person or couple will have different needs and expectations.

- We strongly suggest using a comparison tool;LifeDirect is the most extensive and offers quotes from multiple leading life insurers such as Cigna, AIA, Fidelity and others. All have strong credit ratings, meaning the insurers will pay if you or your family need to claim. And, should you need to claim, LifeDirect handles that too by liaising with the insurer.

Life Insurance Policy Business Definition

Source: https://www.moneyhub.co.nz/life-insurance.html

0 Response to "Life Insurance Policy Business Definition"

Postar um comentário